Travel Insurance Covered by Your Credit Card: What to Know

Find out what travel insurance your credit card covers abroad and whether it provides enough protection for medical emergencies, cancellations, or lost luggage.

The visa isn’t the only travel document you may need for international trips. Some countries, like Saudi Arabia, require proof of travel insurance as part of the visa application process. The good news? Most bank-issued credit cards include travel insurance benefits.

What exactly does travel insurance entail when bundled with a credit card—and is it enough to travel confidently abroad?

What Is Travel Insurance?

Travel insurance is a policy, purchased from an insurer, bank, or travel company, that provides compensation or support if something goes wrong during your travels overseas. While coverage varies widely between plans, most travel insurance policies share three core protections:

Overseas medical costs. Reimbursement for emergency medical care and hospital stays abroad.

Emergency assistance. Evacuation or repatriation to your home country due to illness, injury, or death while traveling, or in response to a qualifying domestic crisis.

Foreign liability coverage. Replaces your domestic liability policy when you’re abroad.

Travel insurance isn’t mandatory for most trips, but a handful of countries—including Algeria, China, Cuba, and Russia—require it so they’re not left covering your medical bills. Some long-term visas, like Working Holiday or digital-nomad visas, also require travel-insurance attestation.

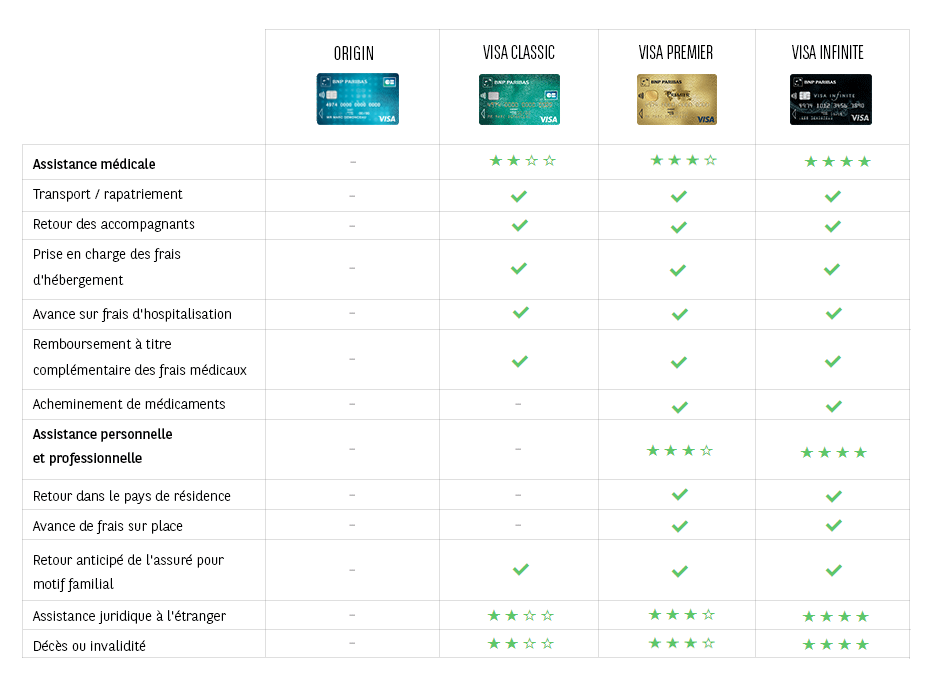

Credit-Card Travel Insurance: What’s Covered?

Even though travel insurance is often optional, it adds peace of mind—hence the close link between credit-card products and travel protection. Bear in mind, though, that basic cards usually come with limited coverage, so pairing your card with a dedicated travel-insurance plan is often wise.

With most standard-issue credit cards, the built-in insurance is basic. It’s easy to activate: just pay for your trip using the card while it’s valid and in good standing, and you’re covered outside your home country. But lower-tier insurance often means:

low medical-cost caps; possibly nothing toward flight cancellations

little or no reimbursement for lost luggage

If you want stronger safeguards—higher coverage limits, flexible trip-cancellation terms, free virtual doctor visits, and so on—you’ll likely need supplemental travel insurance. Talk with your banker to review your current card’s travel-insurance details.

A specialist in regulatory monitoring and a content destination expert, she analyzes daily changes in entry formalities to turn complex administrative processes into practical guides. Her role blends ground-level expertise with technical precision to ensure the reliability of the information provided to travelers.

Get our visa news first in your Google results: add Visamundi to your preferred sources.